By Staff Writer, PHCC-National Association

Key Takeaways:

- Labor Markets Will Cool in ’26, But P-H-C Demand for Talent Remains

Employment growth is expected to continue slowing in 2026 as the unemployment rate approaches 5 percent. However, labor demand among P-H-C businesses is expected to persist as a large share of the workforce nears retirement and the pipeline of younger workers remains thin. Labor shortages continue across the broader construction market, with roughly half of employers reporting difficulty finding skilled applicants. - Modest But Uneven Growth in Construction Demand Expected

Construction activity in 2026 is projected to expand at a modest but uneven pace, with strength concentrated in data centers, select infrastructure programs, and renovation activity rather than broad-based new construction. Residential remodeling and upgrades to existing housing stock are expected to remain steady, with roughly 2 percent growth as homeowners prioritize energy-efficiency improvements and system replacements over new builds. Against a backdrop of still-elevated interest rates, labor constraints, and materials volatility, contractors should expect targeted opportunities alongside continued margin pressure. - The Buzz Around AI Will Continue as Businesses Search for Efficiencies

More home-service professionals are experimenting with AI and identifying ways to integrate it into daily operations. The most common use cases include generative AI for content and administrative tasks, AI-enabled marketing and review management tools, and platforms that improve scheduling, customer responsiveness, and operational visibility. - Declining Interest Rates Will Support the Industry’s Consolidation Trend

Consolidation activity across HVAC and plumbing service contractors continued in 2025, driven largely by private equity and strategic buyers seeking firms with diversified mechanical capabilities. Looking ahead to 2026, consolidation is expected to persist as platforms pursue broader geographic coverage, with scaled contractors offering multiple service lines remaining the most attractive targets.

Balancing Headwinds and Pockets of Strength

Over the past year, contractors faced mounting pressures from quote volatility, higher material costs tied to shifting tariffs, and supply uncertainty amid the transition to R-454B refrigerants. Residential construction weakened sharply while nonresidential activity saw modest gains driven by AI-related data center investment, though overall U.S. engineering and construction spending is estimated to have declined by 1 percent in 2025.

As we look forward to 2026, the U.S. economy is expected to slow but remain positive as the lingering effects of higher tariffs and policy uncertainty weigh on investment and trade while pockets of strength, notably continued tech and AI investment, support activity. Most major forecasters project modest growth, gradually easing inflation, and a Fed shifting toward a less restrictive stance as rates drift lower through the year. Against this backdrop, contractors may face a mixed environment: resilience in select commercial projects, counterbalanced by ongoing material-cost pressures, supply constraints in some specialty inputs, and softer overall demand that could continue to squeeze margins and stress pricing dynamics.

Labor Outlook

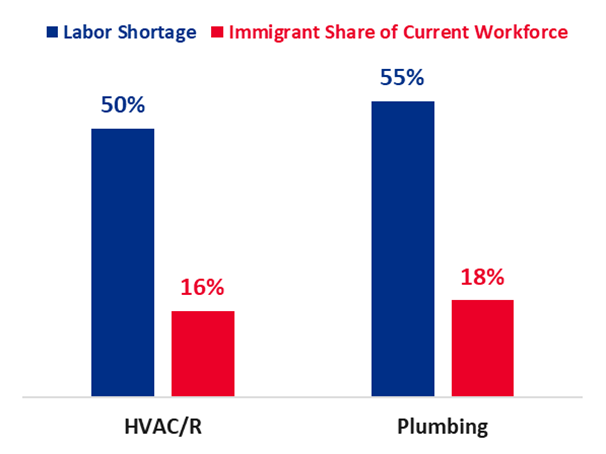

Labor shortage & immigrant labor in HVAC/R & Plumbing. Source: National Association of Home Builders.

Even with stable or moderate economic growth projections, the broader labor outlook suggests mounting challenges could be ahead. Many seasoned construction workers are nearing retirement, and the pipeline of younger entrants remains thin, with only a small share of job seekers expressing interest in the field. Recent industry assessments also point to widening gaps between available positions and the number of qualified workers in key trades. Data from the National Association of Home Builders shows that labor shortages remain widespread across construction trades, including HVAC and plumbing, where roughly half of employers report difficulty finding skilled applicants. As shown in Figure 1, nationally, these trades also rely heavily on foreign-born workers, who make up a meaningful share of the current workforce. As immigration-related enforcement efforts continue to evolve, the sector may experience added strain if changes reduce the availability of workers who currently help support these already tight labor markets.

Occupational Variables

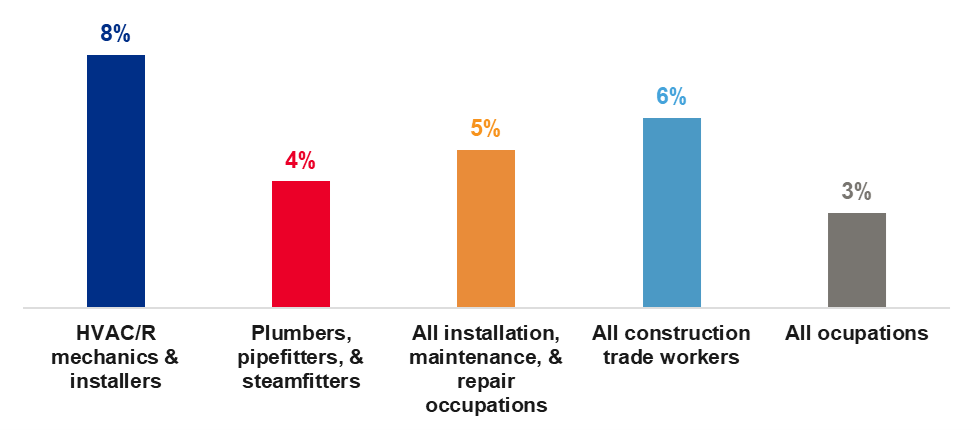

Plumbers, pipefitters, and steamfitters; and heating, air conditioning, and refrigeration (HVAC/R) mechanics and installers form the backbone of the industry, delivering essential installation, maintenance, and modernization services across residential and nonresidential buildings. As aging infrastructure and ongoing construction sustain demand, employment trends in these skilled trades remain a key indicator of the sector’s capacity to meet future needs.

According to the U.S. Bureau of Labor Statistics, employment of plumbers, pipefitters, and steamfitters is projected to grow 4 percent from 2024 to 2035, generating about 44,000 annual job openings largely due to retirements, while HVACR mechanics and installers are expected to see faster growth of 8 percent, with just over 40,000 openings per year—highlighting steady demand across both trades and the continued importance of workforce training and apprenticeship programs.

Together, these trends point to a labor market that, while potentially constrained by demographic pressures and training bottlenecks, remains poised for moderate but resilient growth across the skilled trades.

Projected growth of P-H-C occupations, 2024-2035. Source: Bureau of Labor Statistics.

Construction Outlook

Construction activity in 2026 is expected to expand at a modest but uneven pace, with growth concentrated in a handful of high-performing sectors rather than across the industry as a whole. Forecasts from Deloitte, FMI Corporation, and other sources point to continued strength in data centers and select infrastructure programs, while other sectors face a slower, more cautious period. Against a backdrop of still-high interest rates, persistent labor shortages, and ongoing materials volatility, contractors will need to plan for a year defined by targeted opportunities and disciplined risk management.

Residential Construction

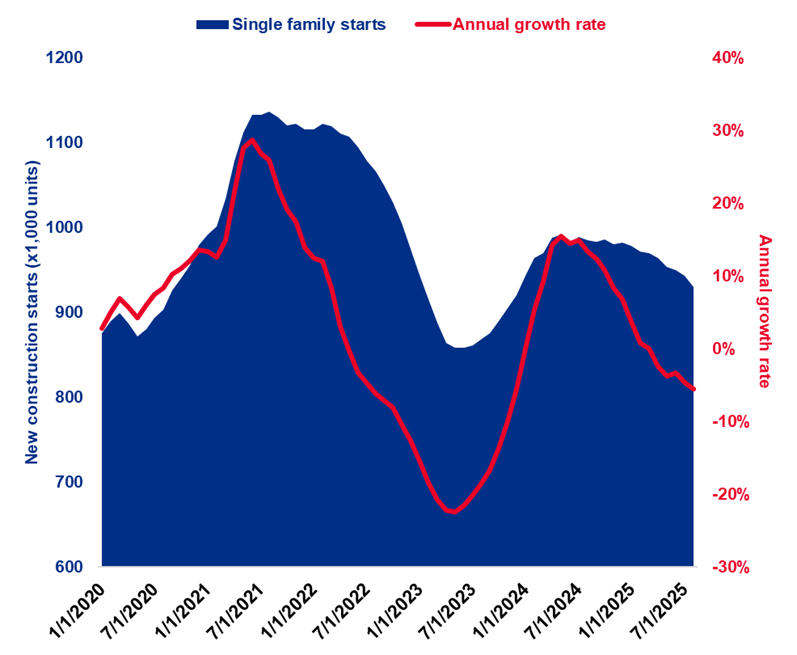

As illustrated in Figure 3 below, U.S. housing starts have swung sharply in recent years, peaking during the post-pandemic surge and declining through 2023 and much of 2024 as high mortgage rates, elevated construction costs, and affordability pressures cooled both single-family and multifamily activity. Although late-2024 brought a short-lived rebound, 2025 brought renewed softening, with builders pulling back amid persistent cost pressures.

Single-family housing starts, 2020 to August 2025. Source: U.S. Census Bureau.

After a pullback through 2024–2025, several industry forecasters expect that lower mortgage rates and improving buyer traffic next year will lift single-family activity, even if supply-chain and labor constraints keep upward pressure on costs. Residential construction should experience a modest rebound in 2026, if financial conditions improve, but the pace of recovery will differ significantly by segment and region.

According to FMI’s North American Engineering and Construction Outlook, single-family residential construction is projected to remain stable, growing by approximately 1 percent in 2026. Similarly, multi-family construction activity is anticipated to remain somewhat stable, with a 2 percent contraction projected for 2026. Additionally, renovation and remodeling of existing housing units are expected to remain steady, with a 2 percent growth rate projected as homeowners continue to invest in upgrades and energy-efficiency improvements rather than pursuing new builds.

Non-residential Construction

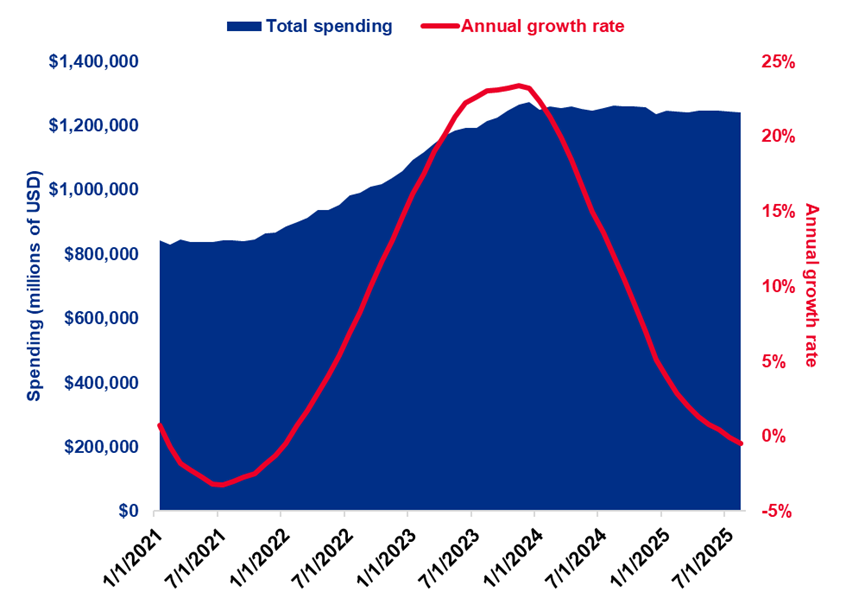

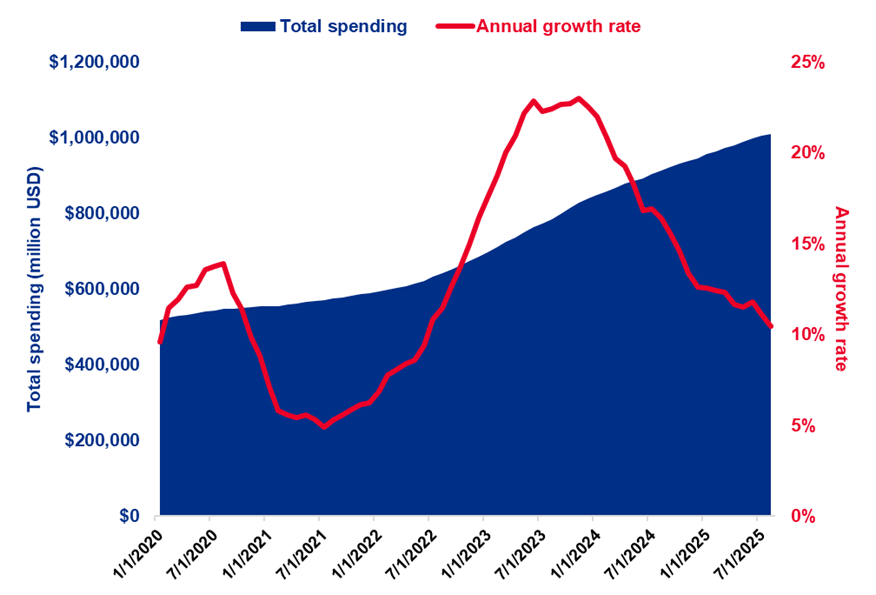

As illustrated below, U.S. non-residential construction spending has followed a pronounced arc over the last five years, surging in the early 2020s on the back of strong industrial, manufacturing, and data-center investment before cooling as higher interest rates and tighter lending standards weighed on project pipelines. While certain categories, like large tech, infrastructure, and manufacturing, continued to provide stability, momentum softened again in 2024 and into 2025 as projects faced rising financing costs, slower demand, and growing caution among owners, developers and financiers.

Total non-residential construction spending in the United States, 2021-2025. Source: U.S. Census Bureau.

As shown in Table 1, FMI’s Outlook shows a mixed non-residential construction landscape, with growth concentrated in a few segments while several others soften or remain flat. Office construction is expected to post one of the stronger gains, driven largely by continued data-center investment, while transportation and healthcare construction work also maintain steady forward momentum. In contrast, lodging and other commercial categories are projected to contract as post-pandemic travel activity normalizes and consumer spending shifts toward essentials, contributing to an overall outlook defined by selective growth.

Non-building Construction

U.S. non-building construction—particularly in water supply and sewage and waste disposal—has experienced notable fluctuations over the past five years. Federal and state funding programs, along with a rise in large natural disaster events, helped sustain momentum during the post-COVID recovery. Growth, however, was tempered in 2024 and into 2025 as higher borrowing costs, supply chain delays, and workforce constraints slowed project starts and extended timelines. In 2025, trends were further influenced by the cancellation or delay of some federal grant and loan programs that had previously supported water and wastewater projects, leading agencies and contractors to exercise greater caution in planning and executing new work. Notwithstanding, the annual growth of the segment remains positive.

Water supply and sewage and waste disposal construction spending, 2020 to August 2025. Source: U.S. Census Bureau.

Looking ahead, FMI’s Outlook projects a 6 percent increase in sewage and waste disposal construction and a 4 percent increase in water supply construction, reflecting continued investment in aging infrastructure and regulatory-driven upgrades. These projections come even as overall industry growth slows compared to the Covid recovery years. With evolving EPA rules, like those related to lead service line replacement, and ongoing needs to modernize treatment plants, many water agencies are still prioritizing critical system repair and expansion.

Key Topics to Watch

Growth of AI

A 2025 survey administered by Housecall Pro of more than 400 home-service experts found that over 70 percent had experimented with AI, including roughly 40 percent of plumbing professionals and 38 percent of HVAC professionals who now use it regularly in their businesses. Among these consistent users, the most common applications include generative AI for content creation and administrative support, AI-driven tools for marketing and online review management, and platforms that streamline operations and provide real-time business insights. Respondents noted that AI is helping reduce routine workload, improve customer responsiveness, and enhance scheduling efficiency, all worthwhile benefits that are encouraging broader adoption across the sector. As AI tools become more integrated into field-service software and equipment platforms, experts expect usage rates to continue rising through 2026.

Closing Out the Refrigerant Transition

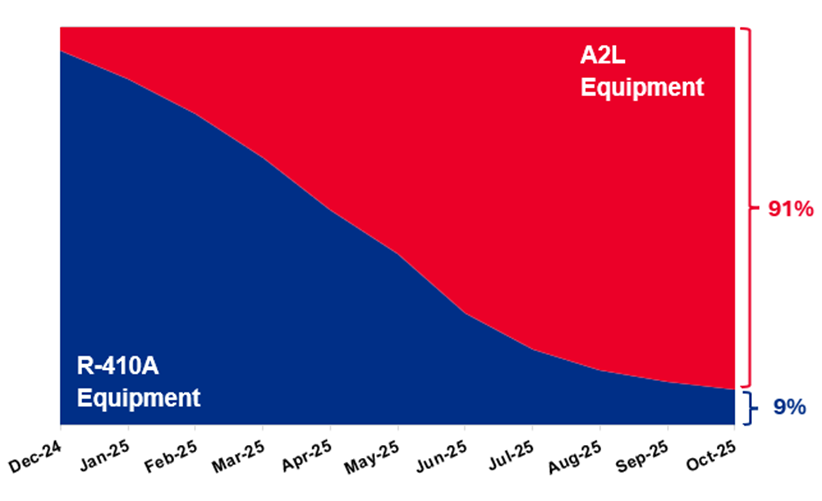

According to HARDI’s Unitary Market Intelligence Report, low-GWP A2L equipment accounted for 90 percent of distributor sales in October 2025, capping a yearlong surge from single-digit adoption levels at the end of 2024. This rapid shift indicates that the industry’s transition to lower-GWP refrigerants is effectively complete. However, P-H-C businesses will still have the opportunity to install R-410A products in 2026 as the EPA has announced changes to its enforcement priorities and will be deprioritizing the enforcement of installation bans on equipment subject to the Technology Transition Rule (TT Rule). In addition to R-410A equipment, other equipment affected by the change in enforcement includes remote condensing units used for commercial refrigeration and cold storage warehouse refrigeration. This announcement provides good news for P-H-C businesses as they enter 2026, pending the agency’s final rule repealing the installation date.

National unitary equipment mixture by refrigerant type. Source: HARDI Unitary Market Intelligence powered by CoMetrics.

BIG Investments in Lead Pipe Replacement

In late November, the EPA announced that it will provide states with $3 billion in new funding, along with $1.1 billion in previously allocated support, to accelerate the removal of lead pipes from homes, schools, and businesses. With states set to deploy these funds toward identifying and replacing lead service lines, plumbing contractors can expect rising demand for inspections, pipe replacement, permitting, and related work. Because lead service line replacement is labor-intensive and requires specialized expertise, contractors who closely track state-level funding plans, grant programs, and municipal capital projects will be well positioned to benefit as these dollars begin flowing into communities in 2026.

Continued Acceleration of Mergers & Acquisitions

In 2025, the consolidation wave continued across HVAC and plumbing service contractor businesses, driven largely by private-equity and other strategic buyers seeking firms that offer combined mechanical, HVAC, and plumbing capabilities. Platforms such as NexCore and PremiStar continued acquiring regional contractors, while many Private Equity (PE)-backed firms pursued add-on deals as part of a key middle-market value-creation strategy. Buyers favored companies with recurring maintenance contracts, strong retrofit demand, and multi-trade service offerings. The year also saw growing tension between consolidators and traditional independents, highlighted by Nexstar Network’s 2025 decision to exclude PE-backed firms from membership, which underscored a widening rift within the trades.

Looking ahead to 2026, industry observers expect continued consolidation as platforms seek broader geographic footprints. Contractors with scale and diversified service offerings will remain attractive targets.

Final Thoughts

As PHCC and its members enter 2026, the construction and trades environment will remain complex, shaped by ongoing labor constraints and selective growth opportunities. Contractors who proactively manage risks, monitor material and labor dynamics, and stay attuned to emerging trends, like AI adoption and federal infrastructure investment, will be best positioned to capitalize on market opportunities. Residential and nonresidential sectors will experience uneven growth, requiring disciplined planning and strategic focus to navigate cost pressures, supply constraints, and evolving customer expectations.

By leveraging technical expertise, multi-trade capabilities, and strategic engagement with industry initiatives, PHCC members can sustain resilience, strengthen operations, and support the broader growth of the U.S. construction and trades ecosystem in 2026 and beyond.